You can find my recent opinion piece for Financial Times Adviser here.

Category: Financial Adviser Blog

Cybercriminals use a wide range of tactics to con people out of their money. Stay one step ahead with these five crucial tips to avoid financial scams.

1. Stay informed

Knowing how to spot a financial scam is your first line of defence. Fraudsters are constantly changing their tactics so regularly educating yourself about common approaches like phishing, identity fraud and romance scams are crucial to staying one step ahead.

Action Fraud and other consumer protection organisations offer a wealth of valuable resources and updates on emerging scams. You could also subscribe to newsletters from trusted financial news outlets like The Financial Times, attend webinars on financial safety, or follow reputable financial organisations on social media.

2. Secure your personal information

Practising good information security is another vital step for warding off financial fraud. Insecure personal information is highly valuable for scammers, and they’ll go to great lengths to acquire it. Implementing strong security practices can significantly reduce the risk that your data will be stolen and used against you.

Use complex, unique passwords for each online account and update them regularly. Enable two-factor authentication wherever possible and be cautious about the personal information you share on social media and public platforms.

Remember to secure your offline data too. Shred documents containing personal information before you bin them, avoid writing your passwords down, and consider keeping important documents in a secure location such as a safe.

3. Do your research

Scammers rely on you taking them at face value. Research the claims made by anyone who contacts you out of the blue, even if they seem legitimate. Genuine organisations will understand if you want to verify the details of a situation.

Unexpected contact, a sudden change of details or time-sensitive opportunities are all indicators of a scam. Search online to see if other people have experienced a similar situation or contact an organisation directly to confirm if the circumstances are genuine. If someone contacts you claiming to work for someone you trust, such as a solicitor or financial adviser, stop the interaction and contact that person directly.

4. Take your time

Criminals want you to act without thinking. They usually try to play on your emotions or rush you into decisions. They may tempt you with time-sensitive opportunities or claim that other consumers are already benefiting from their offer.

Take a step back to assess the situation objectively, do your own research and ask someone you trust for advice. Scammers want you to act quickly and may refuse to provide contact details or threaten to withdraw an offer if you don’t. Remember that if something seems too good to be true, it probably is.

5. Report suspicious activity

If you think you’ve been the victim of a financial scam you should immediately report it to the police. You should also contact your financial institutions to freeze your accounts, seek advice, and potentially prevent fraudulent transactions.

You should still report scam attempts even if you haven’t become a victim of a scam. You can report suspicious activity to Action Fraud and other consumer protection organisations to increase awareness of new scams and criminal tactics.

Contact the police if you think you’ve been the victim of a financial scam. You can also forward suspicious emails to report@phishing.gov.uk and forward suspicious text messages to 7726 for free.

For more information about financial scams visit www.actionfraud.police.uk. If you’re in England or Wales, you can also report fraud or cybercrime to Action Fraud on their website or by calling 0300 123 2040.

Seeking advice on how to look after your money may not be as fun as the immediate thrill of spending it, but it could be a rewarding decision in the long run.

Investing can be a daunting task, especially if you’re not sure where to start, that’s where advice can be handy. A financial adviser can help you understand your financial situation, develop an investment plan, and choose the right investments for your needs to meet your goals.

Value of investment advice

Assess where to invest – Getting advice from a financial adviser can expose you to a wider range of choices when it comes to deciding where to invest. They have the knowledge and expertise on how products work in different markets and can identify any possible downsides as well as potential benefits.

Asset allocation – It’s important to invest in a mix of investments to reduce risk. A financial adviser can help determine your objectives for the investment as well as your attitude to risk before making any recommendations. This is to ensure you are taking the right level of risk and are in a good position to achieve the returns you want.

Portfolio rebalancing – To maintain a healthy mix of investments, you need to rebalance your portfolio. Essentially this is adjusting the weightings of different asset classes in an investment portfolio. A financial adviser will review the portfolio and rebalance where needed to ensure that you don’t take too much risk.

Help achieve your goals – Even a seemingly straightforward financial goal can involve numerous decisions and a range of different products and providers. A financial adviser can help assess what is realistically possible and create a tailored financial plan to ensure you achieve your investment goals.

The key benefits of investing

It’s important to think carefully about putting some of your income aside for the future. For example, you may have more money to invest once your children have moved out, or your mortgage repayments may have reduced. So, what are the benefits to investing?

- Long-term returns

Investing offers the potential opportunity for long-term returns. The money you invest has the potential to grow significantly over time.

- Building wealth

Investing money in a variety of assets can be a great way to potentially build your wealth. The earlier you start and the more you’re able to save, the better shape your financial assets are likely to be in when you need to draw on them.

- Planning for retirement

No matter your age, it’s important to start saving for retirement as early as possible. Investing can help to grow your savings to ensure you have the money to get through your retirement years comfortably.

- Meeting financial goals

Another benefit to investing is the ability to achieve your personal and financial goals. Whether it’s saving for university, buying your dream home or simply building savings for the future, investing can grow your money giving you financial freedom to achieve your goals.

We’re here to help

We can go through the options available to you and discuss the various factors that could affect your investment and provide a personalised, tailored investment plan with the right products for you. Get in touch today.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Key Takeaways:

- With financial uncertainty nowadays, advisers can help you create a plan to profit in the good times and weather the storm against any possible downturns.

- Financial advisers can help you choose the right investments to suit your needs.

- Set clear investment goals and monitor progress when saving for the future.

- The earlier you start saving, the better shape your financial assets are likely to be in when you need them.

- The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Approved by The Openwork Partnership on 23/07/2024.

Saving for your child’s university education requires careful planning and budgeting. By starting early, considering investment opportunities, encouraging your child to save, looking for scholarships and bursaries, and planning, you can make saving for university a manageable goal and give your child the best possible start in life.

What is the cost of university?

It costs roughly £66,560 to go to university in the UK. This figure comes from tuition fees costing most students £9,250 a year. As most courses last around 3 years, this amounts to around £27,750 over the course of their time at university.

As well as a tuition fee loan, students can get a maintenance loan to help cover living costs like accommodation, travel, food, and books. The average maintenance loan is approximately about £6,116 a year, so there will more than likely be a significant shortfall that parents will need to cover. However, the exact cost of university can vary depending on where your child studies and the course they choose.

It’s important to consider the following when saving for your child’s university education.

Start early

How you save for your child’s university costs will depend on how long you’ve got before the money will be needed. For example, if your child is due to start university in the next few years, sticking with cash savings is likely to be your best option so the money is readily available and there’s no investment risk.

Consider Investing

Investing some of your savings can help you achieve higher returns, but it also comes with higher risks. It’s important to understand what investment options you have before making any decisions. These options include:

- Stocks and Shares ISA – A tax-efficient investment account that can help make your money work harder. Unlike a cash ISA, a stocks and shares ISA gives your money more potential to grow by investing it in a range of places like shares, funds, investment trusts and bonds, instead of keeping it in cash.

- Junior ISA – Junior ISAs have a tax-free allowance of £9,000 per tax year, which can be invested in cash, stocks and shares, or a combination of both. The funds in a Junior ISA are locked in until the child reaches the age of 18, at which point the account will convert to a standard adult ISA.

Encourage your child to save

Teaching your child about the importance of saving and encouraging them to save for their own education can help reduce the financial burden on you. Encourage them to take on part-time work and save some of their earnings towards their university education. They can use the following to help them save:

- Regular Savings Accounts – Many banks and building societies offer savings accounts for you to set up on a child’s behalf. Regular savings accounts are designed to encourage children to save an amount every month, and often run for a set amount of time.

- Instant Access Savings Account – Instant access savings accounts allows you or your child to withdraw or deposit money at any time.

Scholarships, Grants and Bursaries

Each university offers their own scholarship, grant and bursary programmes to help students pay for their education. Different universities offer different financial aids, so it is worth doing your research beforehand. Your child may be eligible for financial support based on academic or sporting achievements.

Plan Ahead

Creating a financial plan and setting goals can help you stay on track and make saving for your child’s university education more achievable. Work out how much you need to save, how much you can realistically contribute each month, and how long it will take to reach your goal.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Approved by The Openwork Partnership on 22/05/2024

The effect of psychology on investors

You should base financial decisions on logic and facts. But psychology can have a much larger effect than you think, and it can lead to you making decisions that aren’t right for you. Read on to find out more about what behavioural finance is and how it could affect you.

“Behavioural finance” was first coined in the 1970s by economist Robert Shiller and psychologists Daniel Kahneman and Amos Tversky. They used the term to refer

to how unconscious biases and previous experiences affect the way people make financial decisions.

It can be used to explain why investors can make knee-jerk decisions or invest in opportunities that aren’t in their own best interest. Rather than relying purely on facts, investors often have biases thataffect how they react to certain situations.

Finance bias can lead to “irrational” decisions through shortcuts

There’s a reason why people often make decisions based on biases: they can make the decision-making process quicker.

If you imagine how many decisions you need to make every single day, it’s easy to see why this kind of decision-making can be useful. From what to eat for breakfast to which way totravel to work, it’d take up all your time if you carefully went through the facts for each decision you make. So, you make shortcuts by using biases.

However, while it can be a useful process in your day-to-day life, bias can have a negative effect when you’re making important decisions, including financial ones.

Behavioural finance covers five concepts:

1. Mental accounting

Mental accounting can be incredibly useful when you’re managing a budget. However, inflexibility could mean you miss out on opportunities. The concept refers to how people may designate money for certain purposes. So, you may have different savings accounts for various goals. It’s a process that can help you manage your

outgoings and work towards goals. However, it can also lead to irrational decision making. You may not dip into a savings account that you’ve allocated to buying a newcar even when you face an emergency and it’d make sense logically. How you receive the money may also affect how you use it. For instance, you may put off using money thatwas given as a gift in an emergency because you believe it should be used for something special.

2. Herd behaviour

Herd behaviour is something that’s often seen in investing. When you hear that lots of people are selling certain stocks or buying a specific share, it can be easy

to be led by this and follow suit. It can lead to you making decisions that, while possibly right for others, don’t suit you or your circumstances. It’s not just investing where herdbehaviour can have an effect. You may be tempted to purchase an item after a friend has or choose a savings account because someone you know has.

3. Anchoring

When you have some information, you may focus on this – anchoring your views to this data. Setting a benchmark can be useful, but it can mean you don’t take in

other information, especially if it’s contradictory. So, you may hold on to investments even after the value has fallen because you’ve anchored its worth to a previous valuation.

4. Emotional gap

Emotions often play a role in financial decisions. You may sell a stock because you fear that the price will fall, or make an impulse purchase because you’re happy.

Being comfortable with your financial plan is important, but an emotional gap can fuel irrational decisions as you’re more likely to overlook data.

5. Self-attribution

This concept refers to how investors are likely to have overconfidence in their abilities. You may believe you can reliably time the market to maximise profits when

the markets are unpredictable. In this case, it’s common to see “wins” as being down to your knowledge, while “losses” are attributed to things

outside of your control.

Unconscious bias may affect your decisions in ways you don’t expect. If you have any questions about your finances and the decisions you need to make, please contact us.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

OW4262

Expires 13/03/25

Approved by the Openwork Partnership on 14 March 2024.

At 12.30pm today, Chancellor of the Exchequer Jeremy Hunt announced the UK Spring Budget, as well as the economic and fiscal forecast by the Office of Budget Responsibility.

These legislative announcements are game-changers for Britain’s economy, and Hunt’s announcements included a number of sweeping changes that could potentially affect the personal finances of everyone living and working in the United Kingdom.

In laying out the Spring Budget, Hunt reinforced the government’s dedication to building the British economy while also helping working families.

Hunt’s last announcement, made back in November, included boosts to minimum wages, an increase in State Pension, and a reduction to the headline rate for National Insurance. As of today, the government is maintaining their low-tax strategy by decreasing National Insurance even further, alongside major initiatives aimed at helping drivers, families, those in debt, and other crucial economic groups.

So, ultimately, who wins and loses? Who will benefit? Who will miss out? We’re breaking it all down in this post.

The Winners

Employees

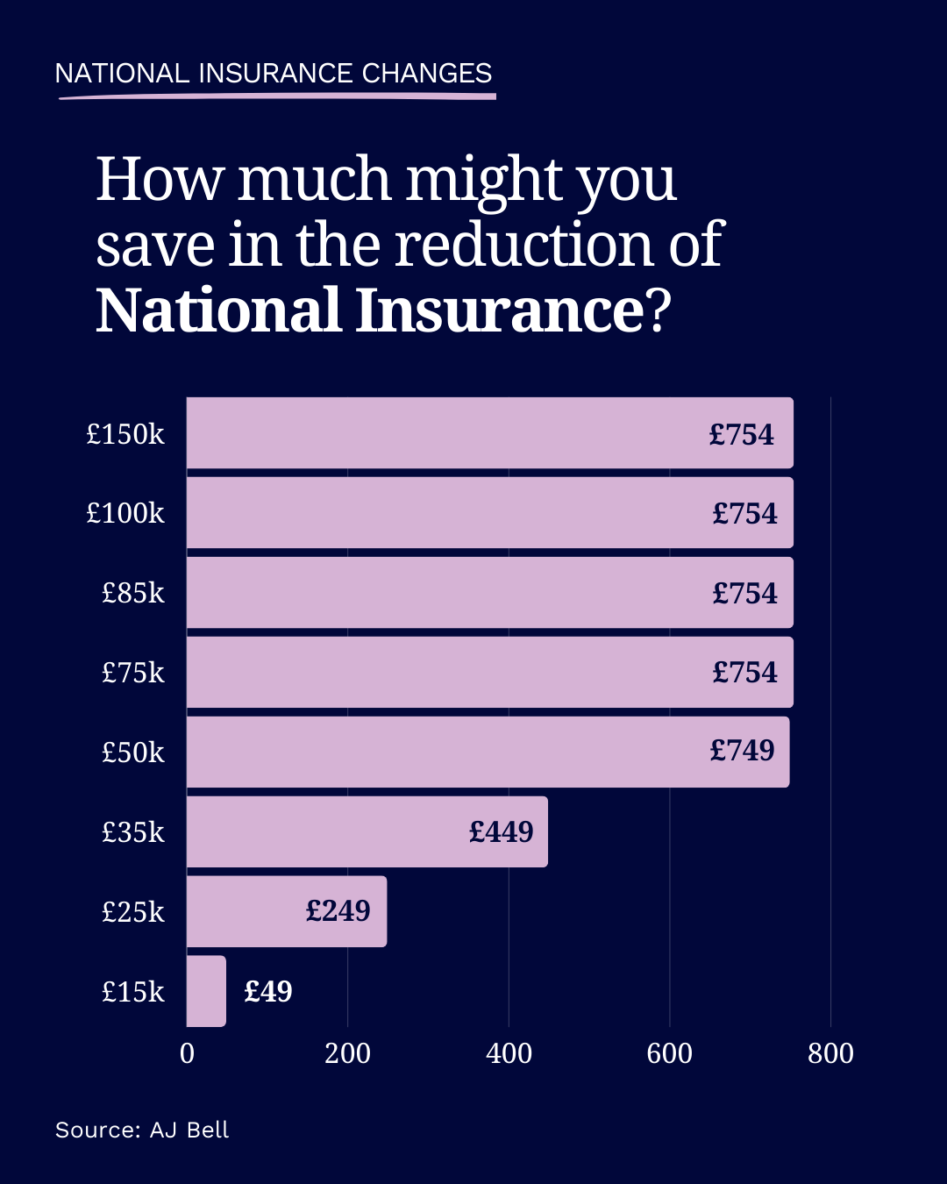

Perhaps the most notable development from the Spring Budget announcement was the continuing drop in the main rate of National Insurance.

Referring to the tax increases for higher-income individuals, Chancellor Hunt stated that: “because we’ve asked those with the broadest shoulders to pay a bit more, today I go further. From April 6th, employee National Insurance will be reduced by another 2p, from 10% to 8%.”This is in addition to the reductions from November’s Autumn Statement, when the rate was brought down from 12% to 10%.

The cut is primarily aimed to benefit employees instead of employers. For example, today’s reduction would be worth around £450 for someone on a full-time salary of £35,000. However, think tanks warn that tax cuts that lack a highly specific target may do more harm than good.

The Institute for Public Policy Research (IPPR) says the cut would cost the government around £10.4 billion, and although that money would then be divided amongst taxpayers, it’s unlikely to end up in the hands of those that need it most. Since high-income individuals benefit most from National Insurance cuts, almost half of the money would go to the richest 20% of households, while only 3% would benefit the poorest 20% of families.

While a National Insurance cut would increase annual household disposable income, the IPPR warns that the negative impact on public services negates this benefit.

Families claiming child benefit

Around 500,000 families will gain almost £1,300 from an increase in the high-income threshold for child benefit. Hunt says he will change the way child benefit is paid. At present, high-income thresholds only apply to individuals as opposed to households, which is set to change.

However, as the transition would take a significant amount of time to enact, the Chancellor announced an immediate solution by increasing the higher income threshold from £50,000 to £60,000.

First-time home buyers

Hunt claimed that the government is on track to deliver over a million homes, opening up the property market and helping young people get onto the property ladder. More than £188 million has already been allocated to building new homes, and over £242 million is still to be spent on building homes across London.

In addition, Hunt stated that a higher rate of property capital gains tax is to be reduced from 28% to 24%, in a bid to increase revenues by increasing the rate of transactions.

Drivers

Fuel duty has been frozen at 52.95 pence per litre since 2011. When the Ukraine War threatened to send prices skyrocketing, a temporary 5-pence reduction to fuel duty was introduced in 2022 to balance things out.

That reduction was extended in 2023. But it has now been extended yet again by Jeremy Hunt in today’s budget announcement, preventing a 13% increase in fuel duty according to the chancellor. Scrapping the increase could cost the government around £2 billion, according to independent think tank Resolution Foundation. While obviously benefiting drivers and the UK industry in general, the plan could have notable climate consequences.

Arts, the media, and the film industry

To help maintain creative sector growth in the UK, the Chancellor has announced a wave of tax relief measures for the British film industry. For example, the rate of tax credits for visual effects studios will be increased, and a 40% tax relief on gross business rates for eligible film studios in England until 2034 was announced. Additionally, the budget included a new tax credit for UK independent films made with a budget under £15 million.

Hunt also announced £26 million in maintenance funding to the National Theatre, and stated that the tax relief for theatres will be made permanent. The relief rate now sits at 45% for touring and orchestral productions, and at 40% for non-touring productions.

Households on universal credit

The Chancellor also announced plans to assist households currently living on universal credit, by making loans easier to repay.

Hunt stated: “Nearly one million households on Universal Credit take out budgeting advance loans to pay for more expensive emergencies like boiler repairs or help getting a job. To help make such loans more affordable, I have today decided to increase the repayment period for new loans from 12 months to 24 months.”

Hunt also announced that he would also abolish the £90 Debt Relief Order charge, and extend the Household Support Fund — aimed at supporting local councils in helping families with food banks and vouchers — for an additional six months.

The Losers

Holiday home landlords

The chancellor claimed that he intends to scrap tax breaks that make it more profitable for second homeowners to let out their properties to vacationers, rather than those who let their properties to long-term tenants. As such, the government is set to abolish the furnished holiday lettings regime.

Vapers and Smokers

The Chancellor also announced a new tax on smoke-free heated tobacco products — set to take effect from October 2026 — following on from the government’s proposed vaping crackdown announced in the autumn. Hunt also announced a one-off increase in tobacco duty. This means that taxes on tobacco products will rise further, making the habit far more expensive.

Oil and Gas Companies

Chancellor Hunt has announced an extension of the windfall tax on oil and gas companies. This means the government will apply the tax for another year beyond the previous end date. Instead of concluding in March 2028, it will continue on into March 2029, raising £1.5 billion.

The windfall tax (more accurately known as the 2022 Energy Profits Levy) is a response to the soaring profits oil and gas companies began making after the combined impact of the lifting of COVID-19 restrictions and price increases due to Russia’s war in Ukraine. The 35% tax (originally 25% but raised in January 2023) applies to any profits made from the extraction of UK oil and gas.

Non-Domiciled Residents

The Chancellor also announced that rules over the taxation of non-dom residents — those who live in the UK but keep their permanent, registered place of residence abroad — are set to change. Hunt stated that the existing system will be replaced by a: “modern, simpler and fairer” one, as of April 2025. From then on, non-domiciled residents living in the UK will face the same taxes as other UK residents after four years.

What’s Next?

As you can see, the 2024 Spring Budget statement has unveiled a number of key initiatives aimed at growing the economy, supporting business, and boosting industry across the nation.

It’s clear that these new initiatives will have a major impact on the finances of British people, and businesses operating in the country. It’s vital, therefore, to seek sound financial advice based on the adaptations laid out by the budget. Indeed, it can be tricky to understand exactly how the Spring budget will affect you or your enterprise without consulting qualified financial advisors first.

So, if you want more information on how the Autumn budget could affect your finances, don’t hesitate to get in touch now.

The value of investments and any income from them can fall as well as rise, so you may not get back the original amount invested.

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Approved by The Openwork Partnership on 06/03/2024

As a parent, you want to do everything you can to ensure that your children have a bright and secure future. One way to do this is by investing on their behalf. Not only can they start adulthood with some savings, but getting children involved early with saving also helps them learn important lessons about money.

The earlier you start investing, the better. Time is a powerful tool when it comes to investing, and the longer you have, the more time your money has to grow. Even if you can only contribute a small amount each month, starting early can make a big difference in the long run.

What investing opportunities are available?

In the UK, there are numerous different ways to invest in a child’s future. The main ones are:

- Junior ISA – Junior Individual Savings Accounts (JISAs) are a tax-efficient way to invest for your child’s future. Junior ISAs have a tax-free allowance of £9,000 per tax year, which can be invested in cash, stocks and shares, or a combination of both. The funds in a Junior ISA are locked in until the child reaches the age of 18, at which point the account will convert to a standard adult ISA.

- Savings accounts – Many banks and building societies offer savings accounts for you to set up on a child’s behalf. You can start an account with as little as £1 for any child aged up to 18. There are two types of savings accounts: regular and instant access. Regular savings accounts are designed to encourage children to save an amount every month, and often run for a set amount of time whereas instant access allows you or your child to withdraw or deposit money at any time.

- National Savings and Investment (NS&I) Premium Bonds – NS&I Premium bonds are investments placed in a savings account that allows penalty-free withdrawals. There is no interest earned, instead the interest rate funds are placed in a monthly draw and any prize won is tax-free.

- Self-Invested Personal Pensions (SIPP) – Your child’s retirement may seem a world away, but you could consider opening a SIPP to invest for their future. Parents can benefit from the tax relief associated with SIPP as they can invest up to £2,880 each tax year with a 20% government top up. This amounts to the £3,600 annual contribution limit.

- Child Trust Funds (CTFs) – Even though Child Trusts Funds (CFTs) are no longer available, you can still contribute up to £9,000 a year into an existing CTF account. If a child was born between 2002 and 2011, they might have a Child Trust Fund. These can be transferred into a Junior ISA.

It’s important to remember that investing is a long-term game, and that staying consistent with your contributions will pay off in the long run. Even if you can only contribute a small amount each month, it’s better than nothing. Consistency is key when it comes to building wealth over time.

https://vimeo.com/openworkltd/download/825110694/ed7dd55f

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Please click here to see the 2024 investment outlook from OMNIS Investments.

In this guide, we explore saving and investing. Starting with the main differences between the two approaches to help you work out which route is best for your money.

What are the differences?

- Saving

Cash savings accounts are ideal if you’re setting aside money you’ll need to access, which will accumulate interest at a rate set by your provider. You will always get back at the very least what you have put into your account, as well as any interest on your deposits. Although cash savings accounts accumulate interest, as a long-term strategy, you could risk losing out on potentially higher returns available from investing, while also struggling to keep up with inflation since cash accounts generally don’t pay very high rates of interest. You will also need to shop around to find the best deals.

2. Investing

When you invest your money, you buy financial assets that you expect to produce a profit or income. Your investments will rise and fall over time and there is a chance you could lose some of your initial investment.

“Although cash savings accounts accumulate interest, as a long-term strategy, you could risk losing out on potentially higher returns available from investing.”

What are the different types of investments?

The main types of asset classes that you can choose as an investor are equities, bonds and property. Each has different levels of risk and return. Safer assets tend to deliver lower returns, while riskier ones can offer the potential for higher returns.

- Equities

Also known as stocks and shares, equities are issued by public limited companies and can be bought and sold on stock exchanges. When you buy an equity, you are buying a piece of that company and become a shareholder. Equities can make you money through increases in the price and you can receive income in the form of dividend payments. The disadvantage is that returns are not guaranteed, and the share price could fall below the level that you invested. Therefore, you may get back less than you invested.

- Bonds

Sometimes called fixed income investments, most bonds are issued by governments and companies looking to raise money. A bond is essentially a loan made to a company or a government by an investor for a set period – usually a number of years. In return, they pay you a regular income in the form of interest over the life of the bond, after which they must repay your loan. Bonds can offer stable returns and are often lower risk than equities, although they tend to offer lower returns in the long term.

- Property

This could be investing in a private property or a commercial type like retail, industrial or office space – through investment funds. Property could make a good long-term investment and is effective at beating inflation. However, it comes with risks, including potentially falling in value or finding yourself unable to sell your investment if market liquidity is low.

POP OUT BOX

Did you know?

At the March 2023 budget, the Help to Save scheme was extended in its current form by 18 months until April 2025. The scheme offers working people on low incomes in receipt of certain benefits, four-year savings accounts with a 50% government bonus where they can save a maximum of £50 a month.

Set your saving goals

Short term

Cash for

Essentials

Medium term

Holidays,

Education

Long term

Retirement,

financial freedom

Why it’s important to diversify

A diversified approach to your investment portfolio is important because a portfolio that blends different types of investments from different geographical regions tends to deliver better returns over the long term. That’s because at any one time, some will be rising in value to potentially offset any others that are falling in price.

A diversified strategy also tends to be less risky than one that invests in a single asset class. Diversifying your investment portfolio is important to minimise your exposure to risk, as is spreading your investments within the different asset classes.

A financial adviser can help you make sure you’re aware of the risks and the length of time required if you want to invest. A longer timeframe (at least five years) will give your investment more time to recover if there are any sudden market swings.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

POP OUT BOX

How does compound growth work?

Imagine snowball rolling down a hill. It keeps getting bigger because it is building on itself. Compond growth for your investment works in the same way and the earlier you start to save, the greater the effects of compounding. But it only works if you keep the original sum invested.

Compound growth can make a big difference to the value of your pension over time because the interest you earn is reinvested and you then build interest on your new total.

POP OUT BOX

Saving Example

Amount per month: £300

Held in: Current account

Growth: 0%

Total after 25 years: £90,000

Investing Example

Amount per month: £300

Held in: Pension fund

Growth: 6% Compounded annually

Total after 25 years: £209,362.98

Extra £119,362.98

Are you on top of your workplace and state pension?

On average, we’re all living longer. Even those who don’t stop working until they are 70 are likely to have many more years of retirement to fund.

• Since 2012, employees have automatically been enrolled into their workplace pension schemes.

• With a workplace pension, the overall minimum total contribution is 8% of your salary – employees contribute 5% of their salary and employers contribute 3%.

• The most you can currently expect to get from the new UK State Pension is £203.85 per week. You’ll be able to claim the new State Pension if you were born on or after 6 April 1951 (for men) or born on or after 6 April 1953 (for women).

Volatility is a feature of investing and markets have bad months, quarters and years. But the evidence still supports the argument that exposure to the markets can be an effective way to build wealth over time. Speak to your adviser and conduct some research to see which approach is right for you.

Get in touch

Speak to us if you want more information about investing or making more of your pension to help you achieve your financial goals.

Please get in touch to arrange a time to chat.

Approved by The Openwork Partnership on 28.11.2023

Did you know that tax breaks could help boost your salary, savings and investments?

It’s easy to miss out on their full benefits as tax can be complex. But with help from your adviser, you can explore the following tax allowances in more detail.

For married couples or those in a civil partnership

You might be able to take advantage of the marriage tax allowance. It allows one half of a couple who earns less than the income tax threshold (which is £12,570) to transfer up to £1,260 to their higher-earning spouse – who must be a basic rate taxpayer.

Spouses and civil partners can also inherit one another’s estates, without being liable for any inheritance tax (IHT). IHT allowances allow you to pass on up to £325,000 of assets (£500,000 if the estate includes a main residence) tax-free. This means a couple can have a total IHT allowance of £1 million.

Tax-free childcare

Couples who both work at least 16 hours a week normally qualify for tax-free childcare. For parents of children aged 11 or under, the government will add £2 for every £8 they pay into an online childcare account. This can be used for after-school, breakfast and holiday clubs, childminders, nurseries and some sporting clubs. This is capped at £2,000 per child per year (£4,000 if the child is disabled) and the child must be 11 or under (or 16 or under for a disabled child). You won’t qualify if your combined adjusted net income exceeds £100,000 in the tax year.

“…tax can be complex. But with help from your adviser, you can explore tax allowances in more detail.”

ISAs

An ISA allows you to save or invest up to £20,000 tax free annually, whether it’s in a cash ISA or stocks and shares ISA – and also comes with the benefit of being exempt from dividend tax and capital gains tax on all growth.

The lifetime ISA (LISA) can be used by first-time buyers to fund a deposit for a property or taken tax-free from the age of 60. As well as paying interest, each subscription to your LISA benefits from a 25% government bonus (up to a maximum of £1,000). The maximum you can put in each year is £4,000, which comes out of your £20,000 ISA allowance.

The LISA can be opened by anyone aged 18–39, but you can keep saving into it until you are 50.

JISAs

You can also invest up to £9,000 in a Junior ISA (JISA) and save for your child either in a cash JISA, a stocks and shares JISA or a combination of the two. Investments can be made from birth until the age of 18.

“…comes with the benefit of being exempt from dividend tax and capital gains tax on all growth.”#

POP OUT BOX

Four tax breaks that could help you

- Trading allowance

If you’re a basic rate taxpayer and have a side income from a hobby or a casual business like babysitting, gardening or freelancing, you are eligible to earn the first £1,000 tax-free.

- Rent-a-room

If you rent a furnished room in your home to a lodger, the first £7,500 of rent each year is tax free. If you make more than this amount it will need to be included in a tax return.

- Working from home

If you have to work from home because your job requires you to live far away from your office or your employer does not have an office, you may be able to claim tax relief of £6 a week for household costs.

These include things like phone calls or energy bills but not expenses that you would have used anyway as part of your everyday living (like broadband, rent or mortgage).

- Uniform expenses

If your job requires a uniform that you need to clean yourself, you can claim tax relief on what you spend, but the amount varies depending on your job and rate of income tax.

Personal savings

Your annual pension allowance is £60,000, although it can be lower for higher earners and where pension savings have been flexibly accessed. When you contribute to your pension some of the money you would have paid in tax to the government goes into your pension instead For example: If you are a basic rate taxpayer, a £100 contribution will only cost you £80.

Capital gains tax

Profits or gains you make on the sale or disposal of an asset (like a property or shares) are exempt from tax up to the annual allowance threshold which is £6,000 in the current tax year (2023/2024). For married couples or those in civil partnerships who own joint assets, the allowance is £12,000. If you don’t make use of this allowance in a tax year, you can’t carry it over to the next.

Tax and employee share schemes

If your employer offers you company shares, you could be eligible for tax advantages – for example not paying Income Tax or National Insurance on their value. Tax advantages only apply if the shares are offered through the following schemes:

• Share Incentive Plans

• Save As You Earn (SAYE)

• Company Share Option Plans

• Enterprise Management Incentives

You may be offered shares outside of these schemes, but they won’t have the same tax advantages. Your financial adviser is here to help you make the most of your available tax allowances.

Charitable donations

You can donate to charity tax-free and claim back the

tax on your donation through gift aid. If you are a higher or additional income taxpayer, you can also claim back the difference to the basic rate on your gift aid donations.

Just remember to keep hold of all records of your donations to claim tax relief when the time comes to submit your tax return.

POP OUT BOX

Dividends

Dividends are a portion of a company’s profit that they choose to pay shareholders as a reward for their investment. Companies usually pay out dividends twice a year, although some firms will pay out on a quarterly basis.

In April 2023 the tax-free dividend allowance fell to £1,000 and will drop again to £500 in the year after. The tax rate you pay on dividends above the allowance depends on your income tax band, which you can work out by adding your total dividend income to your regular income. If one member of a married couple receives dividends and the other does not, you could transfer shares between you and benefit from two allowances.

Tax-free dividend allowance:

April 2023–2024

£1,000

April 2024–2025

£500

An ISA is a medium to long term investment, which aims to increase the value of the money you invest for growth or income or both. The value of your investments and

any income from them can fall as well as rise. You may not get back the amount you invested.

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Tax concessions are not guaranteed and may change in the future. Tax free means the investor pays no tax.

For specialist tax advice, please refer to an accountant or tax specialist.

Get in touch

Speak to your adviser to help you maximise your earnings and for guidance in areas like pension contributions. Please get in touch to arrange a time to chat.

Approved by The Openwork Partnership on 28.11.2023

Household bills have increased rapidly during the past year. The current cost of living crisis began with the Covid pandemic, causing problems for economies around the world and creating global supply chain delays followed by the war in Ukraine.

Following such an extended period of price rises, you may be concerned about your household finances and long-term plans. If you are retired or about to retire and rely on a defined contribution (DC) pension for your income, read on for five options that could help you make your pension stretch further.

01 Use existing savings for income

If the value of your DC pension has fallen recently, one way to help it to recover could be to keep as much of it invested as possible. Consider whether you could live on less income than you are currently taking.

Using alternative savings or investments could help reduce the amount you need from your pension. By leaving your money invested in your pension, you’ll retain more fund units, which may increase in value when markets recover.

When things are looking better, if you have depleted your emergency fund you could use some of your income to rebuild it gradually. This will provide a buffer to support you if markets drop again in the future.

02 You could take a phased retirement

Many people are choosing to take a phased retirement to fight the effects of the cost of living crisis.

This might include:

• Taking a part-time job

• Setting up your own business or working as a contractor

• Staying in your old job but on reduced hours

Continuing to work means you could contribute more to your pension, helping it to grow further. Keep in mind that the Money Purchase Annual Allowance (MPAA) might limit the amount of tax relief you can receive.

Once you start drawing income flexibly from your pension, you can only receive tax relief on contributions up to £10,000 a year, although you can make contributions over this amount. You could also receive your State Pension payments alongside any income you make from work once you reach State Pension Age. If you are struggling to cover your monthly expenses, this could provide a welcome boost to your income. We can help you understand all the financial implications of phased retirement and pension contributions.

03 An annuity could provide guaranteed annual income for the rest of your life

If you would like a guaranteed annual income but don’t want to go back to work, you could consider an annuity. Buying an annuity with a lump sum from your pension can deliver a guaranteed annual income for the rest of your life. Annuities are becoming an attractive option for retirees again. Rates have risen to a 15 year high in 2023, meaning you can now get much more for your money. For example, in September 2023, a 65-year-old with a pension pot worth £100,000 could secure a guaranteed income of £7,462 a year for life.

04 A lifetime mortgage could free up cash from your home

A lifetime mortgage is a loan that you take out against the value of your home, allowing you to exchange equity for tax-free cash. To be eligible, you must:

• Be over 55 and a UK resident

• Own your home, which must be worth/valued at more than £70,000

• Have little or no mortgage left to pay

A lifetime mortgage has several benefits and disadvantages.

Benefits of a lifetime mortgage:

• You retain ownership of your home

• The cash can be used to pay for anything

• You don’t need to repay the loan, or the interest accrued, until you move into long-term care or pass away

Disadvantages of a lifetime mortgage:

• Interest will be charged on the original loan and the interest accrued, so the amount you owe will grow

• The interest rates on lifetime mortgages tend to be higher than on residential mortgages

• You may have less to leave beneficiaries in your will

05 Downsize your home to reduce monthly bills

Moving to a smaller property with a better Energy Performance Certificate rating could offer a win-win situation. Not only could this help free up some cash from the sale of your old property, but a smaller, more efficient home could also reduce monthly bills.

If you’re worried about the rising cost of living and would like to discuss ways to protect your finances from the effects of inflation, we’re here to help. Please get in touch to arrange a time to chat.

Important Information: The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Past Performance is not a guide to future performance and should not be relied upon. HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes, which cannot be foreseen.

A Lifetime Mortgage is not suitable for everyone and may affect your entitlement to means tested benefits, so it is important to seek financial advice before taking any action. If you are considering releasing equity from your home, you should consider all options available before equity release. The interest that may be accrued over the long term with a Lifetime Mortgage, may mean it is not the cheapest solution. As interest is charged on both the original loan and the interest that has been added, the amount you owe will increase over time, reducing the equity left in your home and the value of any inheritance, potentially to nothing. Although the final decision is yours, you are encouraged to discuss your plans with your family and beneficiaries, as a Lifetime Mortgage could have an impact on any potential inheritance. We would also encourage you to invite them to join any meetings with us so they can ask questions and join in the decision, as we believe it is better to discuss your decision with them before you go ahead.

Approved by The Openwork Partnership on 04.10.2023

Since the government introduced pension auto-enrolment in 2012, millions more workers have started saving for their retirement. Now, the government has confirmed plans to extend auto-enrolment to encourage a savings boost. The changes could have implications for both employees and business owners.

Following a review of auto-enrolment the government has revealed key reforms forecast to increase pension contributions by £2 billion a year.

Key auto-enrolment changes to be aware of

The minimum age of auto-enrolment will fall from 22 to 18

Young workers could start saving into a pension much sooner. The government intends to lower the minimum auto-enrolment age from 22 to 18.

For employees, this could be a positive step. Saving for retirement from the outset of their careers could help establish positive money habits among workers. In addition, compound growth means early contributions have the potential to grow significantly.

For business owners, it could mean their outgoings will increase as they’ll also need to make pension contributions on behalf of eligible workers.

The lower earnings limit will be removed

Currently workers must earn at least £6,240 to be eligible for auto-enrolment. The government plans to remove this lower earnings limit, so workers will receive contributions from the first pound they earn.

This will boost pension contributions among those that are already paying into a pension. It will also mean low-income workers that haven’t previously benefited from a pension, such as those who work part-time while caring for children or older relatives, will automatically start paying into a pension and receive employer contributions too.

From an employer’s perspective, this change could, increase the amount they are contributing to employees’ pensions.

There could be a maximum limit on pension pots

As most employees are entitled to a pension through their employer, frequent job hopping could lead to individuals holding numerous small pensions. This may make it difficult to manage pensions effectively and understand if you’re on track to reach your retirement goals.

The government has set out initial plans to help savers manage multiple pots. Among the proposals is a maximum limit on the number of pensions a person can have. The report also suggests a ‘central clearing house’ to make it simpler to consolidate pensions.

There is no timescale for the proposed changes

The official document does not set out a timescale to implement any of the changes. So, while young and low-income workers are set to benefit from auto-enrolment, it could be several years before they start contributing to pensions.

The minimum pension contribution will not be increased

The government has not made plans to change the current rules for contributions. Currently, the minimum contribution is 8% of qualifying earnings, made up of 5% from employees and 3% from employers.

Research suggests that minimum contribution levels are not enough to afford a comfortable lifestyle in retirement. There have been calls for the government to increase the minimum pension contribution level to help close the gap.

Auto-enrolment won’t be extended to cover self-employed workers

Some organisations have called on the government to extend auto-enrolment to encourage self-employed workers to save for their retirement. However, support for the self-employed has been overlooked in the latest report.

Research from the Institute for Fiscal Studies suggests the number of self-employed workers paying into a pension has fallen over the last decade.

It also found self-employed workers that pay into a pension rarely change the amount they contribute. The analysis suggested a form of auto-escalation, such as a direct debit that increases in line with inflation, could help self-employed workers save more for their retirement.

Take control of your pension and retirement

While the change to auto-enrolment could mean more people are on track for a financially secure retirement, there are still challenges. If you want to reach your retirement goals, engaging with your pension sooner, rather than later, could allow you to identify the steps you need to take.

Please contact us to discuss your retirement aspirations and how we could help you create a tailored financial plan.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Approved by the Openwork Partnership 07/09/23

OW4631

Expiring 5 April 2024